After a lengthy decision-making process, on March 6, 2024, the Securities and Exchange Commission (SEC) announced changes to the climate disclosure rule that will require standardized climate-related disclosures. The SEC now requires companies to disclose certain climate-related information, including material climate-related risks and opportunities, material Scopes 1 & 2 GHG emissions, and certain climate-related financial metrics. Scope 3 emissions have been removed from the rule, but they are still in the emissions disclosure rule passed recently by the state of California.

Today’s final rule is far lighter than the draft requirements published two years ago, but the final rule will still require companies to disclose significant information. According to the SEC, companies will be asked for, at a minimum, the following:

Climate-related risks that have had or are reasonably likely to have a material impact on the registrant’s business strategy, results of operations, or financial condition;

The actual and potential material impacts of any identified climate-related risks on the registrant’s strategy, business model, and outlook;

If, as part of its strategy, a registrant has undertaken activities to mitigate or adapt to a material climate-related risk, a quantitative and qualitative description of material expenditures incurred and material impacts on financial estimates and assumptions that directly result from such mitigation or adaptation activities;

Specified disclosures regarding a registrant’s activities, if any, to mitigate or adapt to a material climate-related risk including the use, if any, of transition plans, scenario analysis, or internal carbon prices;

Any oversight by the board of directors of climate-related risks and any role by management in assessing and managing the registrant’s material climate-related risks;

Any processes the registrant has for identifying, assessing, and managing material climate-related risks and, if the registrant is managing those risks, whether and how any such processes are integrated into the registrant’s overall risk management system or processes;

Information about a registrant’s climate-related targets or goals, if any, that have materially affected or are reasonably likely to materially affect the registrant’s business, results of operations, or financial condition. Disclosures would include material expenditures and material impacts on financial estimates and assumptions as a direct result of the target or goal or actions taken to make progress toward meeting such target or goal;

For large accelerated filers (LAFs) and accelerated filers (AFs) that are not otherwise exempted, information about material Scope 1 emissions and/or Scope 2 emissions;

For those required to disclose Scope 1 and/or Scope 2 emissions, limited assurance of this data;

The capitalized costs, expenditures expensed, charges, and losses incurred as a result of severe weather events and other natural conditions, such as hurricanes, tornadoes, flooding, drought, wildfires, extreme temperatures, and sea level rise, subject to applicable one percent and de minimis disclosure thresholds, disclosed in a note to the financial statements;

The capitalized costs, expenditures expensed, and losses related to carbon offsets and renewable energy credits or certificates (RECs) if used as a material component of a registrant’s plans to achieve its disclosed climate-related targets or goals, disclosed in a note to the financial statements; and

If the estimates and assumptions a registrant uses to produce the financial statements were materially impacted by risks and uncertainties associated with severe weather events and other natural conditions or any disclosed climate-related targets or transition plans, a qualitative description of how the development of such estimates and assumptions was impacted, disclosed in a note to the financial statements.

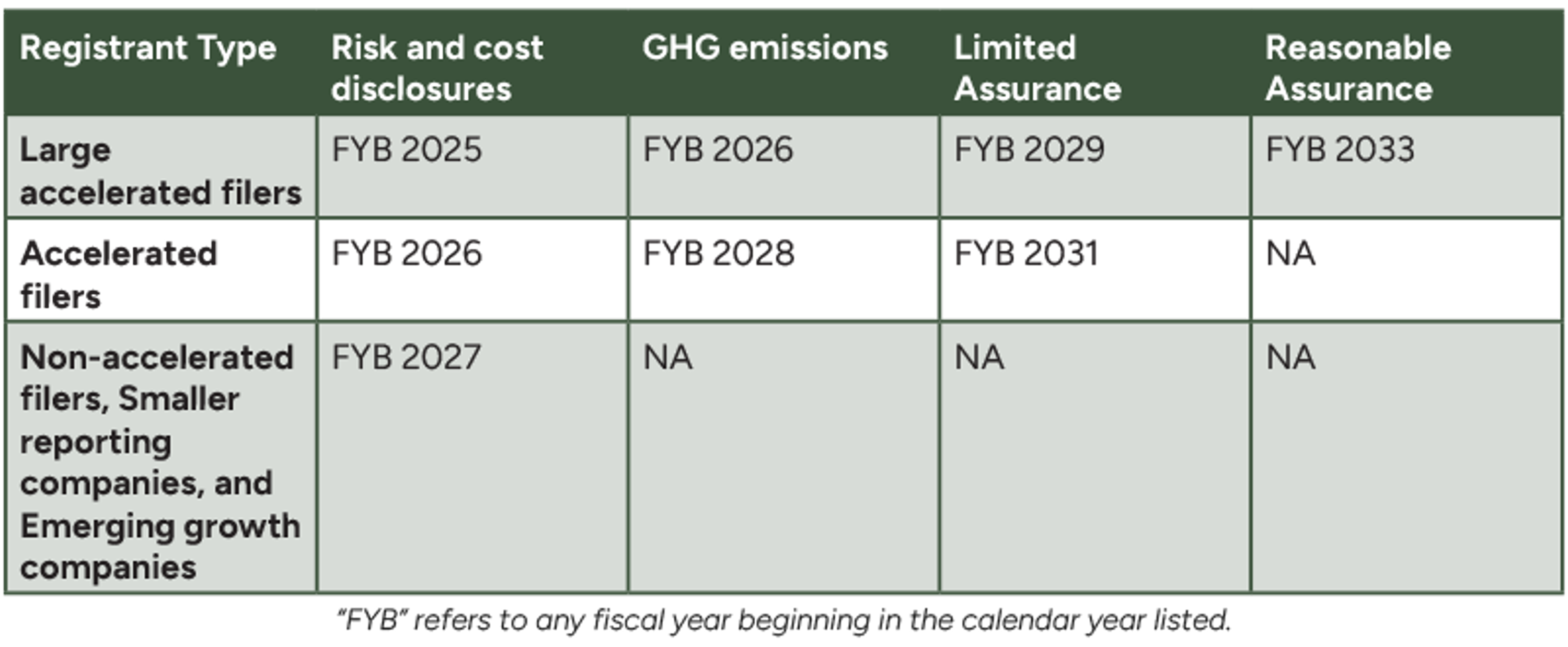

The timing of these requirements varies depending the size of your company, with the earliest reporting requirements expected to begin in fiscal year 2025:

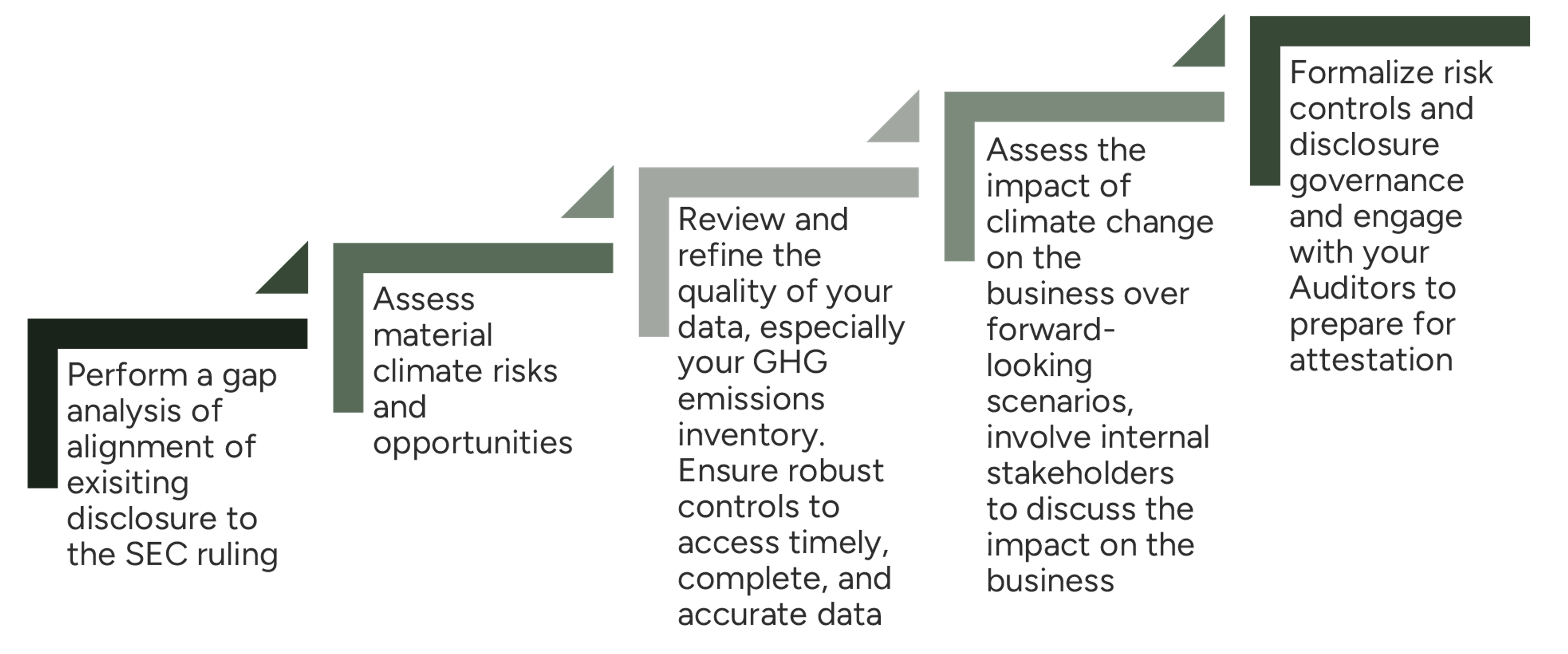

How SLR’s ESG & Sustainability Advisory Team Can Help

This new ruling might mean major changes to your strategy and disclosures. We have been helping companies develop ESG and climate strategies for 25 years and are ready to assist with implementing this new rule in alignment with your needs and requirements. We can help you to:

Recent posts

Insight

10 June 2026

5 minutes read

Planning for a fluorine free future: Transitioning away from PFAS firefighting foams