Gestionar el riesgo climático: una necesidad estratégica para las empresas

by Sofía Díaz , Cristian Rencoret

View post

As the first-ever year of mandatory climate-related financial reporting in Australia comes to an end and the second begins, one recurring theme amongst disclosers has been the effort and complexity required for the scenario analysis component.

The lack of guidance from the government or the Australian Securities and Investments Commision (ASIC), or the often-contradictory stances from auditors hasn’t helped either. The recent launch of the finalised Department of Climate Change, Energy, the Environment and Water’s (DEECCW) National Climate Scenario Guidance is most welcome as it provides much needed clarity for companies moving forward, especially as the assurance requirements over this component of Australia Standard Reporting Standards (ASRS) kick in to gear in Year 2.

Australia’s Climate Scenario Guidance[1] has been finalised to help organisations assess climate-related risks, marking a considerable milestone for climate risk analysis in Australia.

We contributed to the public consultation of this document in January, in which we supported the overall direction, whilst calling for stronger alignment with AASB S2 requirements, greater flexibility for organisations, and more practical support for new or less mature organisations.

The final guidance reflects clear progress and lands at a critical moment, as mandatory climate disclosures come into force, most June 30-ending Group 1 entities prepare to publish their inaugural Sustainability Reports, and Group 2 entities begin gearing up for it. While the direction is strong, many reporters grappling with scenario analysis will still face key gaps in its practical application.

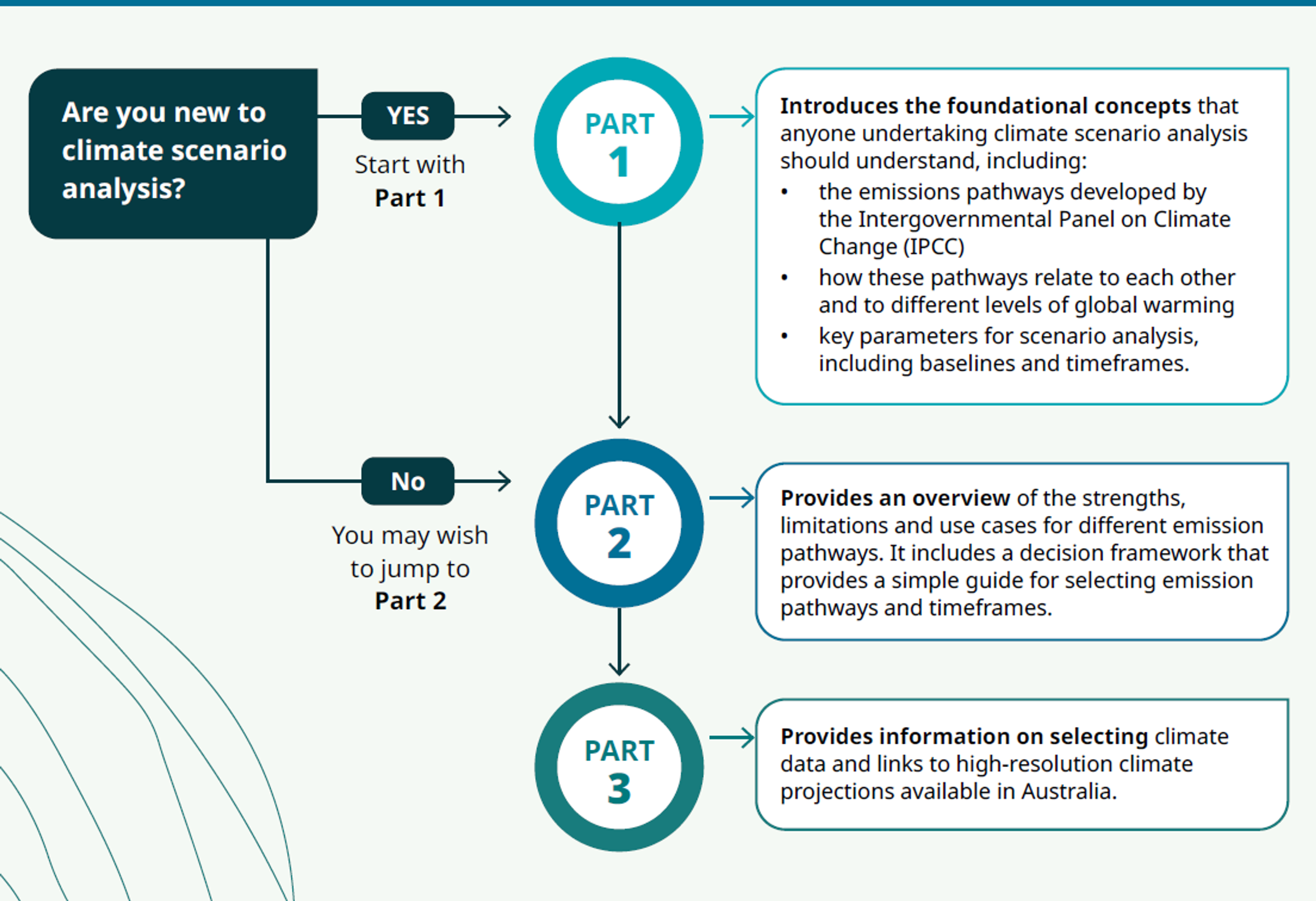

The guidance provides a structured, end-to-end approach to climate scenario analysis, supporting organisations from foundational concepts through to scenario selection and data use. It is explicitly designed to be flexible and applicable across maturity levels, helping both new and experienced users navigate what has historically been a complex process A strong example of this is the report’s structure, with Figure 1 in the guidance (page 4) highlighting where different audiences may derive the most value.

This guidance also more closely aligns with Australia’s evolving regulatory framework and clarifies how it supports compliance with AASB S2 standard (page 5).

While the national guidance does not prescribe how to meet AASB S2 requirements, it provides a critical methodological backbone and reference point for organisations undertaking scenario analysis for disclosure.

One of the most important anchors for scenario selection is Australia’s Climate Change Act 2022, which explicitly links national targets to the Paris Agreement goals, including:

“pursuing efforts to limit the temperature increase to 1.5°C above pre-industrial levels.” [2]

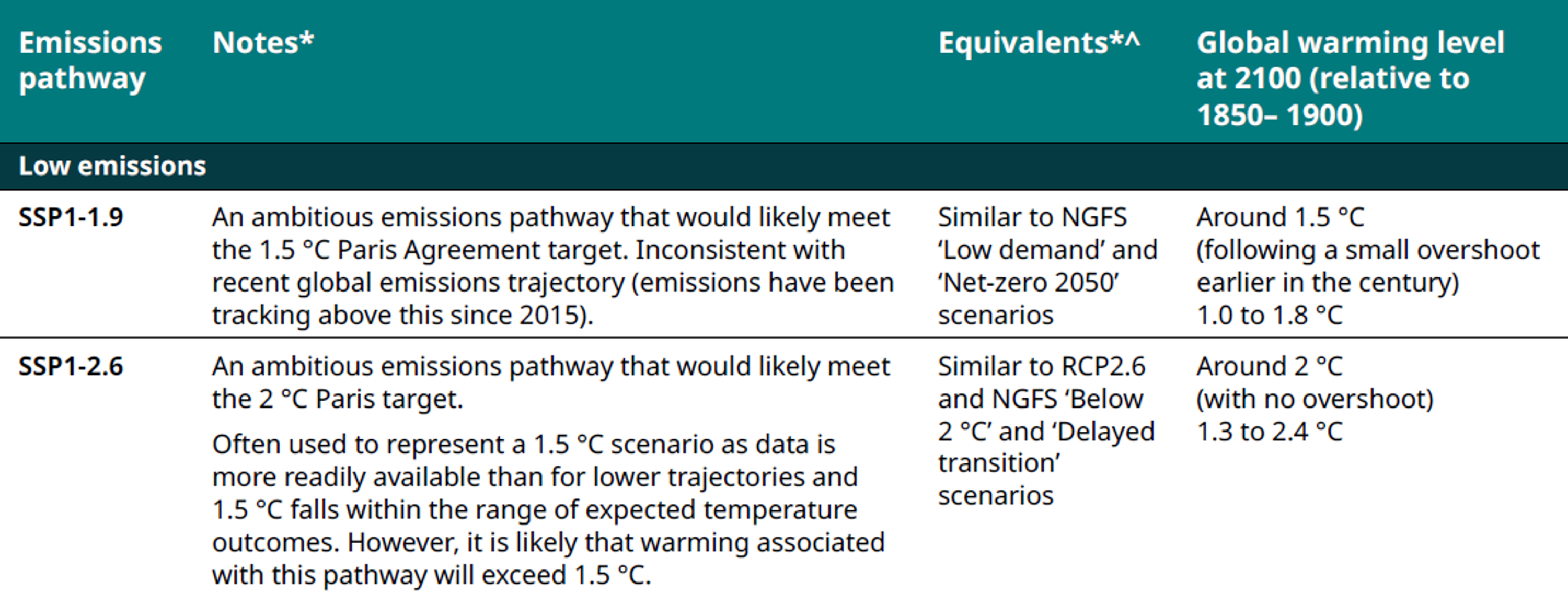

The interpretation of this clause has been inconsistent, with some auditors accepting only the lowest warming scenarios (e.g. SSP1-1.9).

The guidance also helps clarify this, and directly references SSP1-2.6 as an option to represent a 1.5 °C scenario, as data is more readily available than for lower trajectories.

A key strength of the published guidance is its principles-based, flexible approach to:

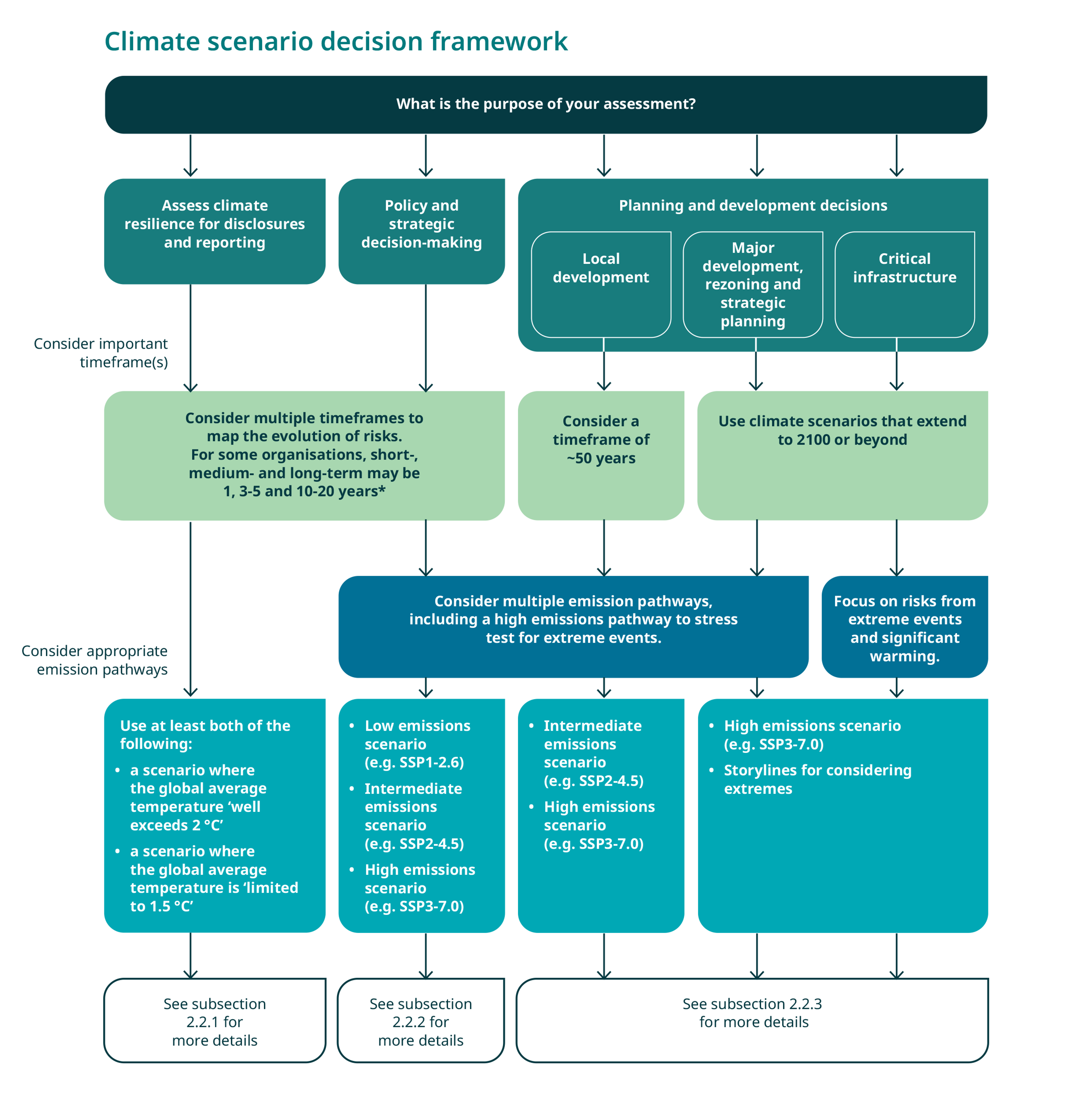

This directly addresses industry feedback and supports more tailored, useful decision analysis. Particularly welcome is the decision framework, which provides a simple guide for selecting emissions pathways and timeframes for use in climate scenario analysis (see page 20 of the guidance).

This decision framework also clearly identifies SSP1-2.6 as a representation of a ‘1.5 °C Scenario’, as data is more readily available than for SSP1-1.9 and 1.5 °C falls within the range of expected temperature outcomes.

However, flexibility does not remove the need for robust justification, and organisations will need to clearly articulate:

While the guidance is very clear that it is not part of the standard, the alignment with AASB S2 is tacit for anyone reading it. To be truly helpful, it should show how to translate scenario analysis into compliant disclosures. Key questions that will remain unanswered for many will likely be:

Climate scenario analysis remains notoriously difficult and, while this guidance is most welcome, many organisations will still need to interpret requirements themselves. For a practical walkthrough of how to implement scenario analysis in line with AASB S2, see our recent webinar.

While the guidance focuses heavily on physical climate risk, it does not offer insight into how to apply scenario analysis to assess transition risks, such as policy, market and technology. Organisations will need to assess both types of risks under the different scenarios, but this is not covered in the guidance.

While the guidance points to SSP1–2.6 as a practical representation of a 1.5°C-aligned pathway, this remains a point of tension in the rollout of AASB S2. The legislative anchor (the Corporations Act referring to the Climate Change Act 2022) mandates alignment with a scenario that is “pursuing efforts to limit the temperature increase to 1.5°C above pre-industrial levels. ”. However, some auditors have a narrow interpretation of this, limiting it to SSP1–1.9, which experts widely regard as ‘dead’[3] . This creates uncertainty for organisations trying to balance data availability, decision-useful insights, regulatory intent, and assurance defensibility.

The release of the guidance is a significant step forward in clarifying what can be an abstract and difficult process for organisations to undertake, but the real challenge now moves to implementation, and that is where SLR can help you.

We have a track record of supporting organisations with:

Catch up on the articles below to learn more about the support and solutions our specialists are providing clients navigating ASRS & Mandatory Climate Disclosures:

Please reach out if you have any questions or want to discuss how to apply climate scenario analysis for your organisation.

Contact Us

by Sofía Díaz , Cristian Rencoret

by Andrew Quinn

by Esther Diffey