Carbon and Energy Newsletter - December 2022

- Post Date

- 16 March 2023

- Read Time

- 6 minutes

This is our final update of the Carbon and Energy newsletter in 2022 and will cover some of the major outcomes that resulted from COP 27, changes to carbon compliance schemes such as the UK Emission Trading Scheme, ESOS Phase 3 and the current trend in carbon pricing. SBTi are also set to release another sector specific set of criteria, this time for steel, which will provide best practise guidance to support its transition to a net-zero economy.

We’ll provide further updates in the 2023, in meantime the team would like to wish everyone a Merry Christmas and Happy New Year!

COP27

COP27 came to a close in Sharm El Sheikh last month, where an emphasis was mostly placed on adapting to climate destruction, above mitigating the global emissions contribution to climate change. There was a notable lack of commitment to phasing out our reliance on fossil fuels for a preferred 1.5⁰C emission pathway, which continues to be led by companies in the private sector who were voicing their commitments at COP27 following schemes such as SBTi – with signups almost doubling since last year’s COP26.

A continuing challenge remains how international climate finance will consider the needs and priorities of developing countries. As part of this, a loss and damage fund has been announced at COP27 which will ensure that the costs associated with the impacts of climate change are spread across the developed world, to support vulnerable countries hit hard by climate disasters. Pledges have currently been made to the Adaptation Fund totalling more the 230 million USD.

UK Emission Trading Scheme

The end of reporting year for UK ETS is almost upon us (31st December 2022), therefore please do not forget to take your end of year meter readings and begin contacting verifiers to verify reports.

For sites operating within the UK ETS ‘opt out’ scheme, the government has confirmed the carbon ‘fine’ price that operators will need to pay if they exceed their allocated 2023 carbon target. This has seen a considerable increase to £83.03/tonne, 58% higher than the 2022 price of £52.56/tonne.

In a recent update, the government has also highlighted an amendment to the Activity Level Changes (ALC) regulation. The amendment will allow operators to apply for data from the 2020 scheme year to be omitted from the 2022 ALC process if installations are able to evidence that discrepancies between reductions in activity levels and correlating emissions were wholly or mainly caused by the COVID-19 pandemic. This should enable impacted UK ETS instillations to avoid a reduction in their free allowance allocation. A threshold of 15% between the reduction in activity and reduction in emissions between the 2019 and 2020 scheme years will be applied.

The evidence required by the operator must contain:

- activity levels and correlating emissions to show that they meet the threshold level

- verified sub-installation attributable emissions data with evidence of verification

- evidence that the reduction in activity, as well as the discrepancy between the reductions in activity and emissions, are due wholly or mainly to the effects of the COVID pandemic

- a statement explaining why, when comparing 2020 to 2019 levels, the emissions attributable to the sub-installation did not fall by at least the same proportion as its activity level (this should also be linked to any changes in production data)

The deadline for applications is 31st January 2023 and each sub-installation will be reviewed separately. If approved, the average activity level will be based on 2019 and 2021, instead of 2020 and 2021. More details can be found here.

Carbon Price

A review of the trends and current costs associated with the UK ETS allowance price shows that prices are currently tracking at an average of around £69.08/tonne – a £1.10 discount to the EU allowance. This is a dramatic change from the observed peaks in August and September at £97/tonne. Further details on the UK Emissions Trading Scheme markets can be found here.

SBTi - Steel Guidance procedures

The Science Based Target initiative (SBTi) is launching a new standard providing a specific set of criteria for businesses in the steel sector. From 23rd November 2022 to 23rd January 2023, SBTi are undertaking a multi-stakeholder consensus to ensure the criteria and guidance for steel companies are robust, clear, and practical - SBTi Steel Public Consultation Feedback Survey. This is aimed to provide a sectoral approach to apply best practice in the steel industry with methodologies, tools and guidance aimed to support a transition to a net-zero economy. Further information and draft documents for the public consultation can be found here. A final version of the SBTi Steel Guidance and Target Setting Tool is expected to go live in Q2 2023.

Climate Change Agreements (CCA)

The end of TP5 reporting is almost upon us, therefore any variations/change of ownership applications (such as facility exits, base year data corrections, etc.) need to be submitted by 31st December. There will also be upcoming requests in the new year to submit TP5 data.

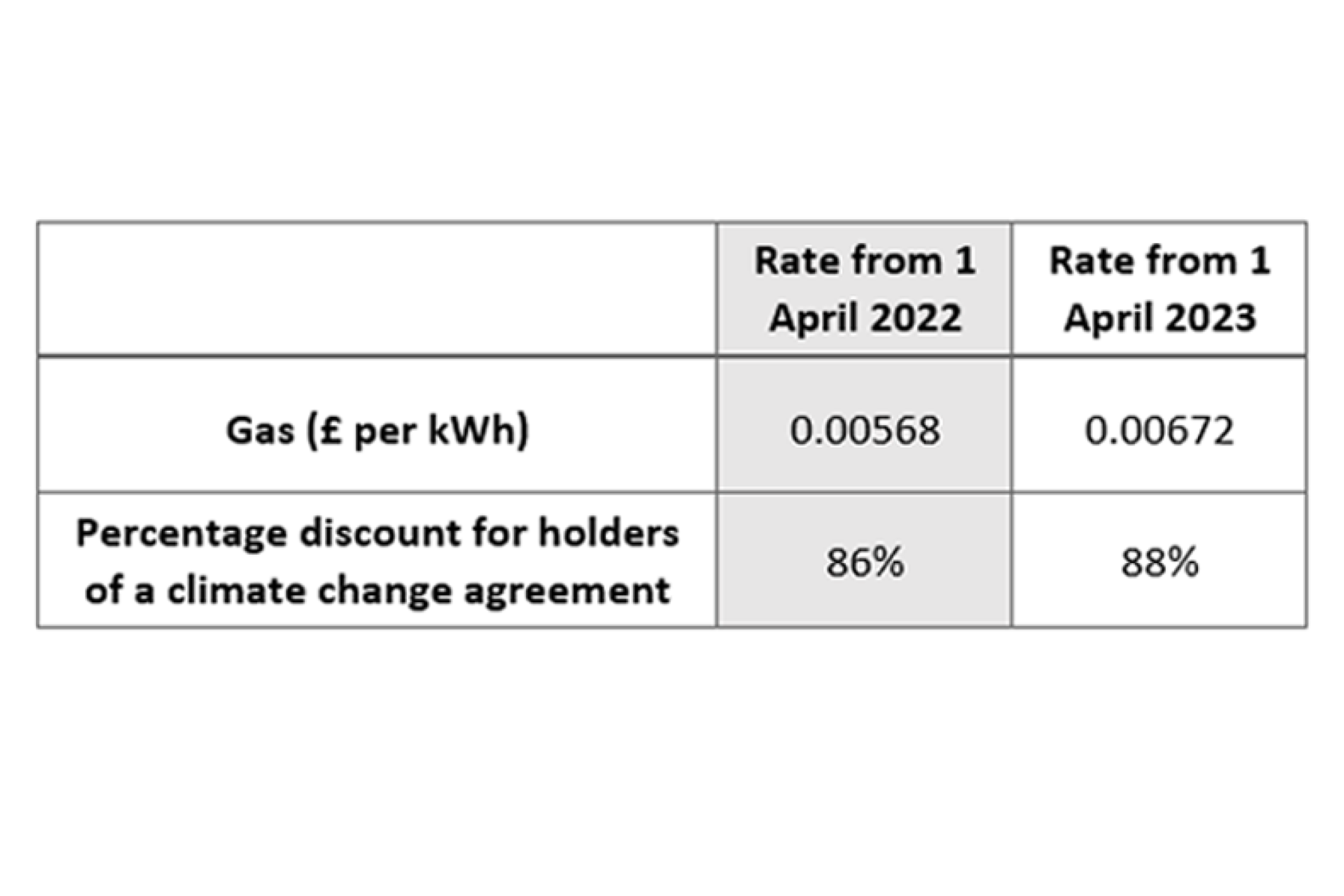

For those who are already in the climate change agreement scheme, in 2023 we expect the Climate Change Levy rate for gas to be further reduced:

Other taxable commodities such as electricity are anticipated to remain the same.

Energy Savings Opportunity Scheme (ESOS)

ESOS phase 3 audits and preparation are fully underway in anticipation for the next compliance deadline of 5th December 2023. A range of changes have taken place which were highlighted our the previous newsletter and summarised below:

- A minimum of 95% of the total energy consumption must be considered rather than 90%

- The addition of an energy intensity metric in ESOS reports

- Requirement to share reports with subsidiaries

- Requirement next steps for information on implementing recommendations and an action plan which will be followed up in ESOS phase 4

- Collection of additional data for compliance monitoring and enforcement

The government also recently published a review of ESOS compliance in Phase 2 audits. The results showed that only 30% of the audits were fully compliant, with the main issues requiring corrective action being:

- Organisation Structure

- Total Energy Consumption & Significant Areas of Energy Consumption

- Sampling Approach and Quality of ESOS Energy Audit

- Energy Saving Opportunities

Full guidance on how to comply with ESOS can be found here.

Greenhouse Gas Protocol

Finally, the Greenhouse Gas Protocol is conducting four surveys to collect stakeholder input which will inform updates or additional guidance related to GHG Protocol’s Corporate Standard, Scope 2 Guidance, Scope 3 Standard, and Market-based accounting approaches. These surveys will be open until 28th February 2023, with stakeholders being encouraged to complete as many surveys as possible which are relevant to their work.

SLR’s Carbon & Energy Management team can provide support in all the above areas. If you need any assistance or require further information, then please contact us.